Editorial Promise

This is not just a story of “bad executives.” It is a corporate-governance case about losses, auditors, directors, banks, advisers, media, markets, and a system that failed to ask hard questions for too long.

SHIMBUN.co.jp does not frame this as a simple foreign hero versus Japanese villains story. The deeper issue is structural: what happens when too many people learn not to ask, not to escalate, and not to break the room’s silence?

数字は嘘をつかない。しかし、数字をどこに置くかで、組織は長く嘘をつける。

The Shape of the Case

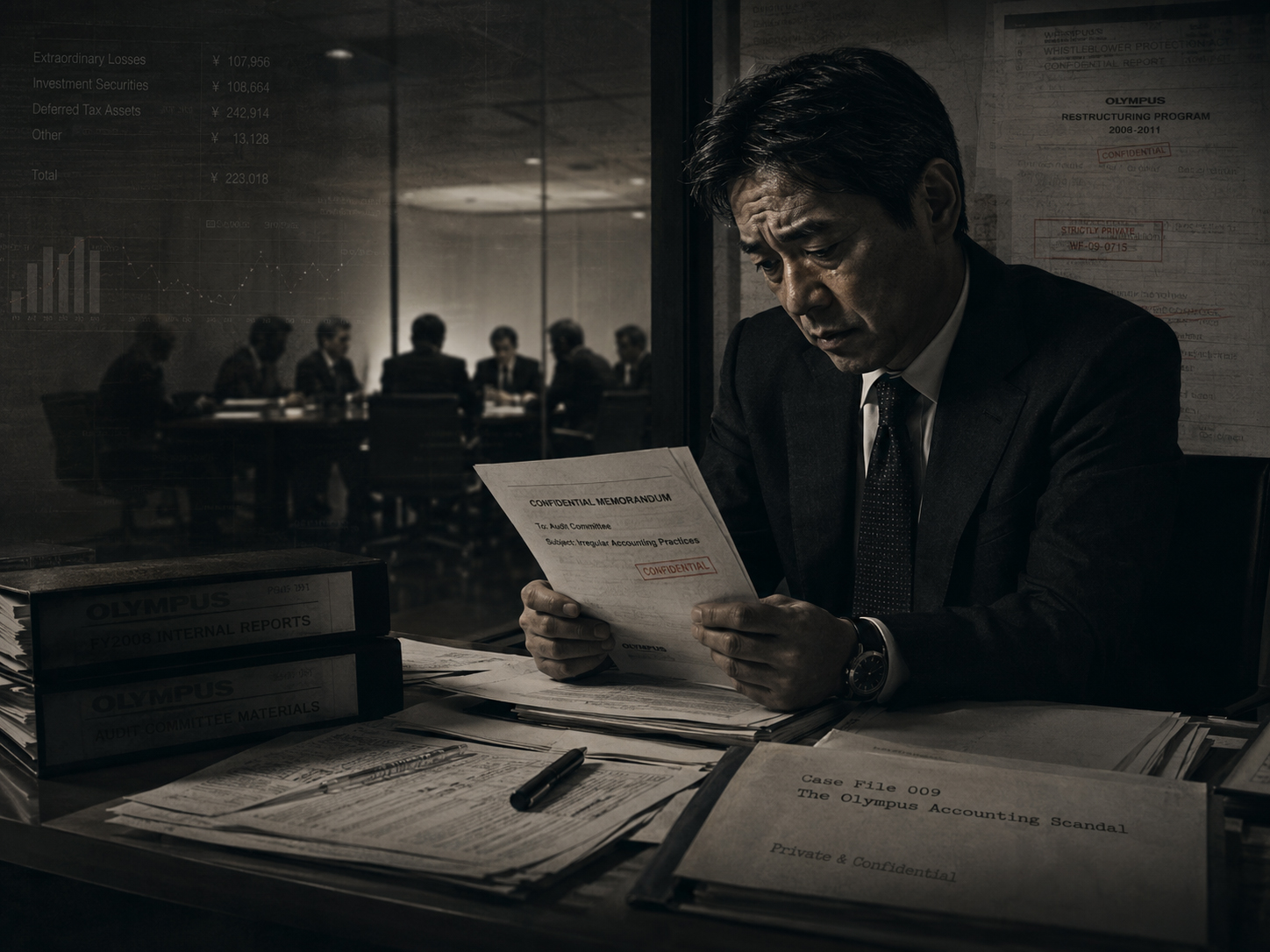

The Olympus Accounting Scandal centered on investment losses that had been hidden or deferred over many years, and on later acquisition and advisory payments that became central to the public explanation of the scheme. The scandal broke open in 2011 after Michael Woodford, newly appointed as president and CEO, questioned suspicious transactions and was removed from his post.

What followed was not only a company crisis. It became a test of Japanese corporate governance, investor trust, audit credibility, press behavior, and the ability of boards to confront unwelcome facts.

Why It Belongs as Case File 009

By Case 008, SHIMBUN had covered organized crime, disaster, terrorism, corruption, justice history, and cold cases. Case 009 moves the archive into corporate Japan and financial deception: the quiet case, the paper case, the boardroom case.

The victims of accounting fraud are not always visible in a single photograph. They include shareholders, employees, counterparties, pension funds, market confidence, and the basic public promise that listed companies tell the truth.

Four archive axes

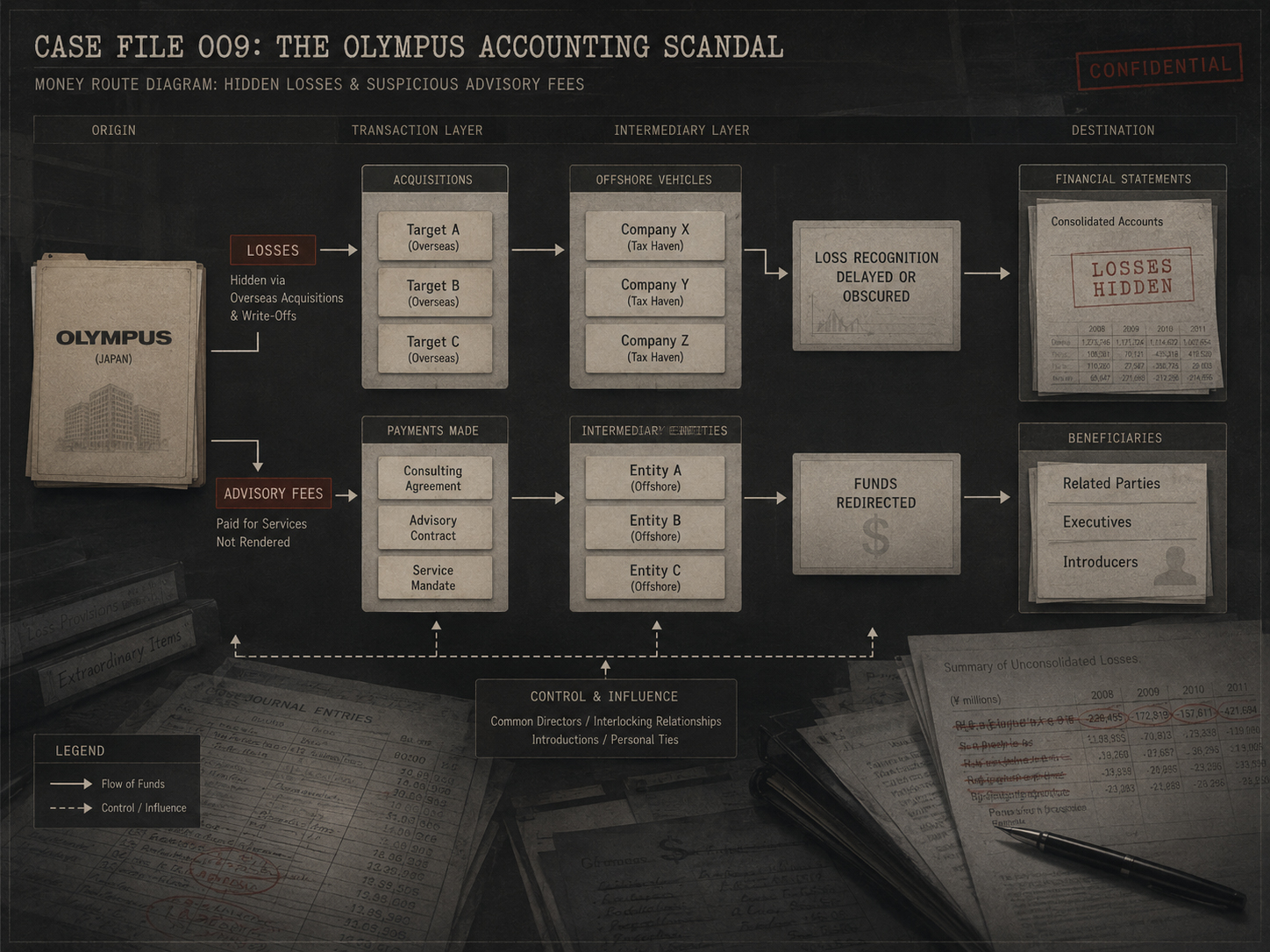

1Loss hiding from the 1990s onward

2Acquisition fees, advisory payments, and money routes

3Woodford’s dismissal and international reporting

4Audit, board oversight, and governance failure

Timeline

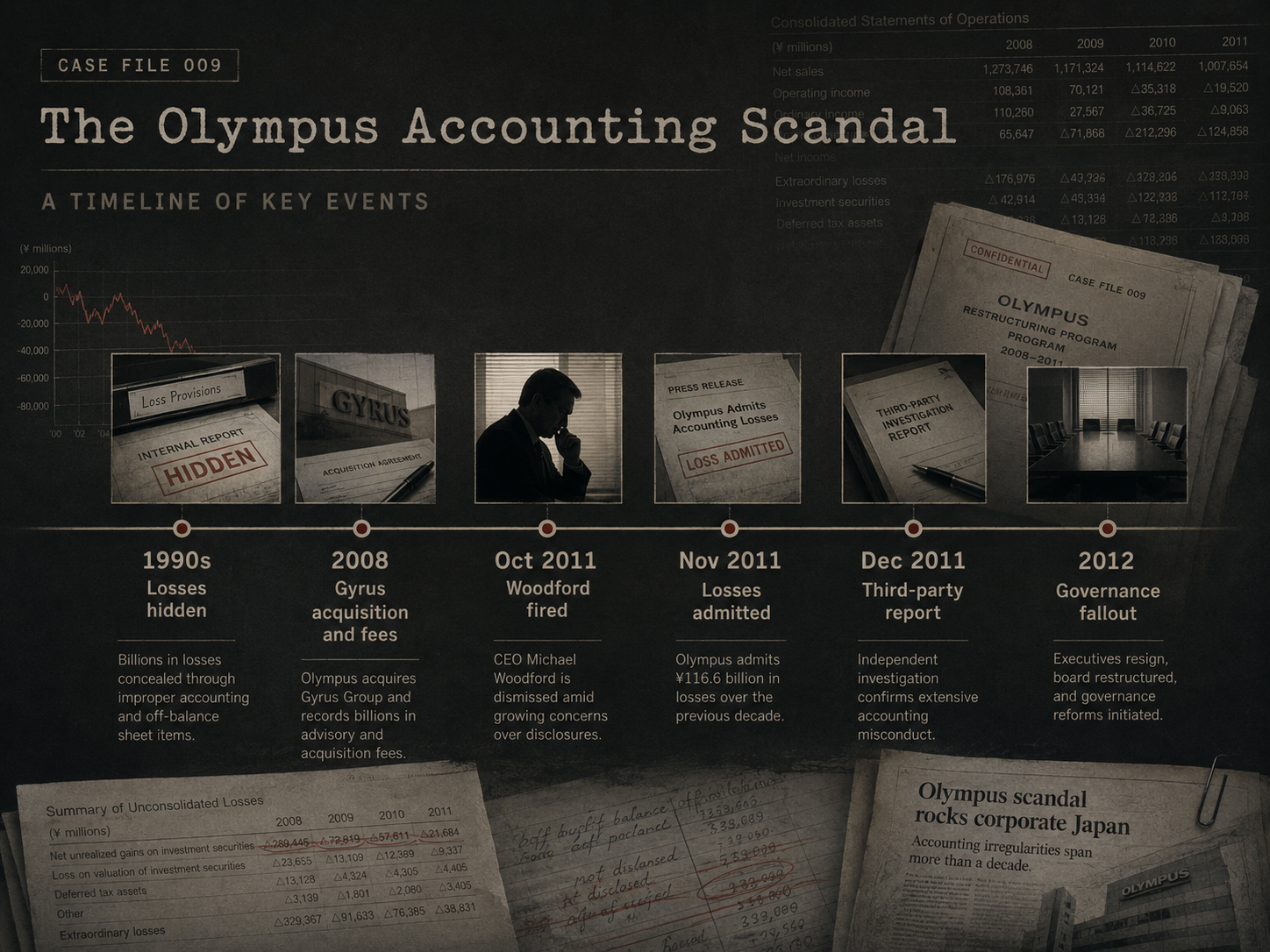

The scandal did not begin in 2011. It unfolded across years of losses, treatments, transactions, questions, dismissal, admission, and investigation.

Investment losses from the post-bubble era are deferred or obscured rather than recognized openly.

Acquisition-related payments and advisory fees later become central red flags.

The CEO is removed after raising questions, drawing international scrutiny.

Olympus acknowledges accounting problems connected to past losses.

An investigation report lays out the scheme and governance failures.

Executives resign, legal and regulatory processes continue, and governance reforms are debated.

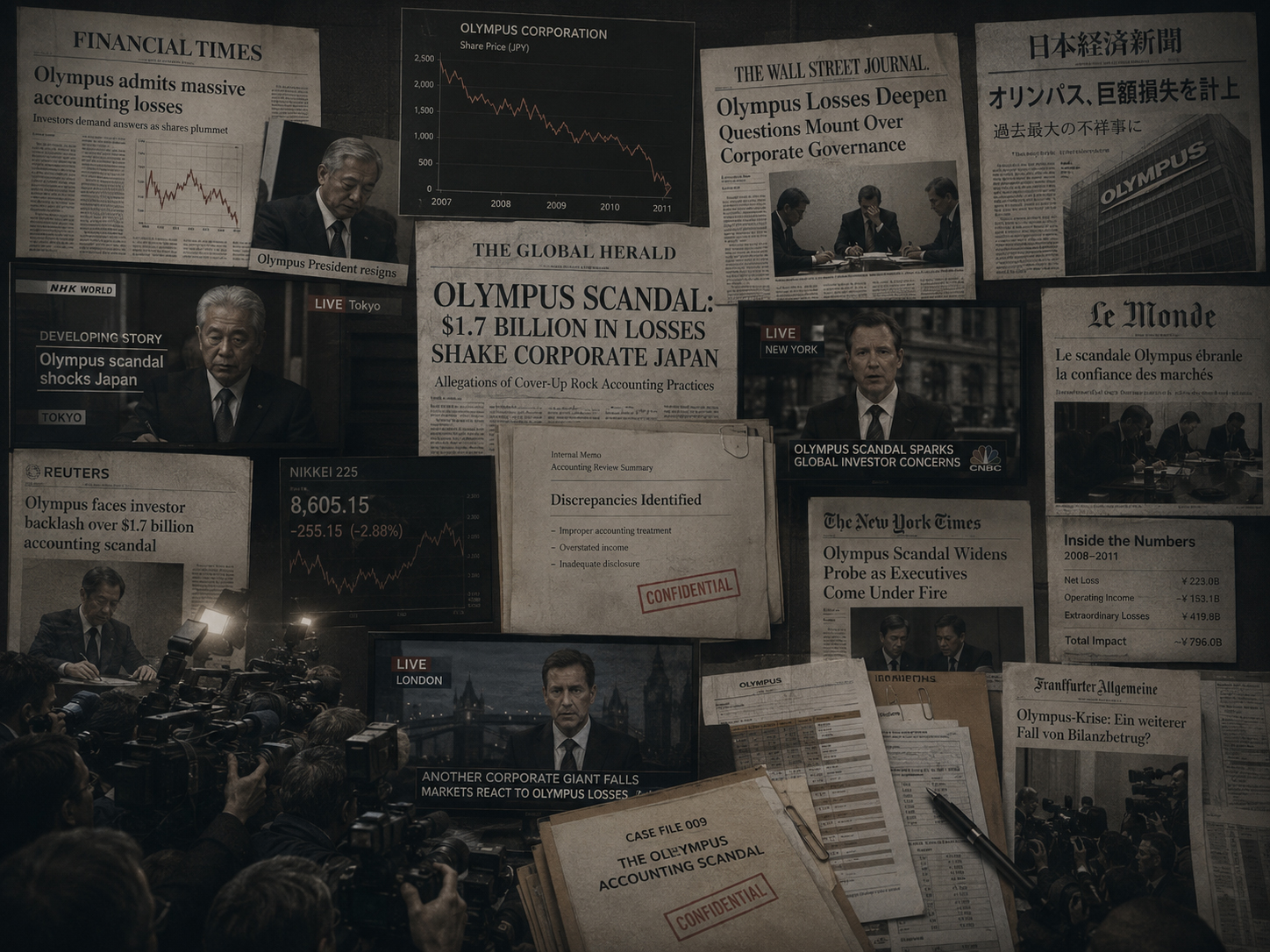

Media and Markets

The scandal also exposed differences in media tempo. International media and investors quickly focused on the scale of acquisition fees and Woodford’s allegations. Domestic reaction was more cautious at first, reflecting the difficulty of challenging a prestigious company without official confirmation.

Markets depend on reliable disclosure. When a listed company’s accounts cannot be trusted, the damage spreads beyond one balance sheet. It touches the credibility of auditors, boards, regulators, and the exchange itself.

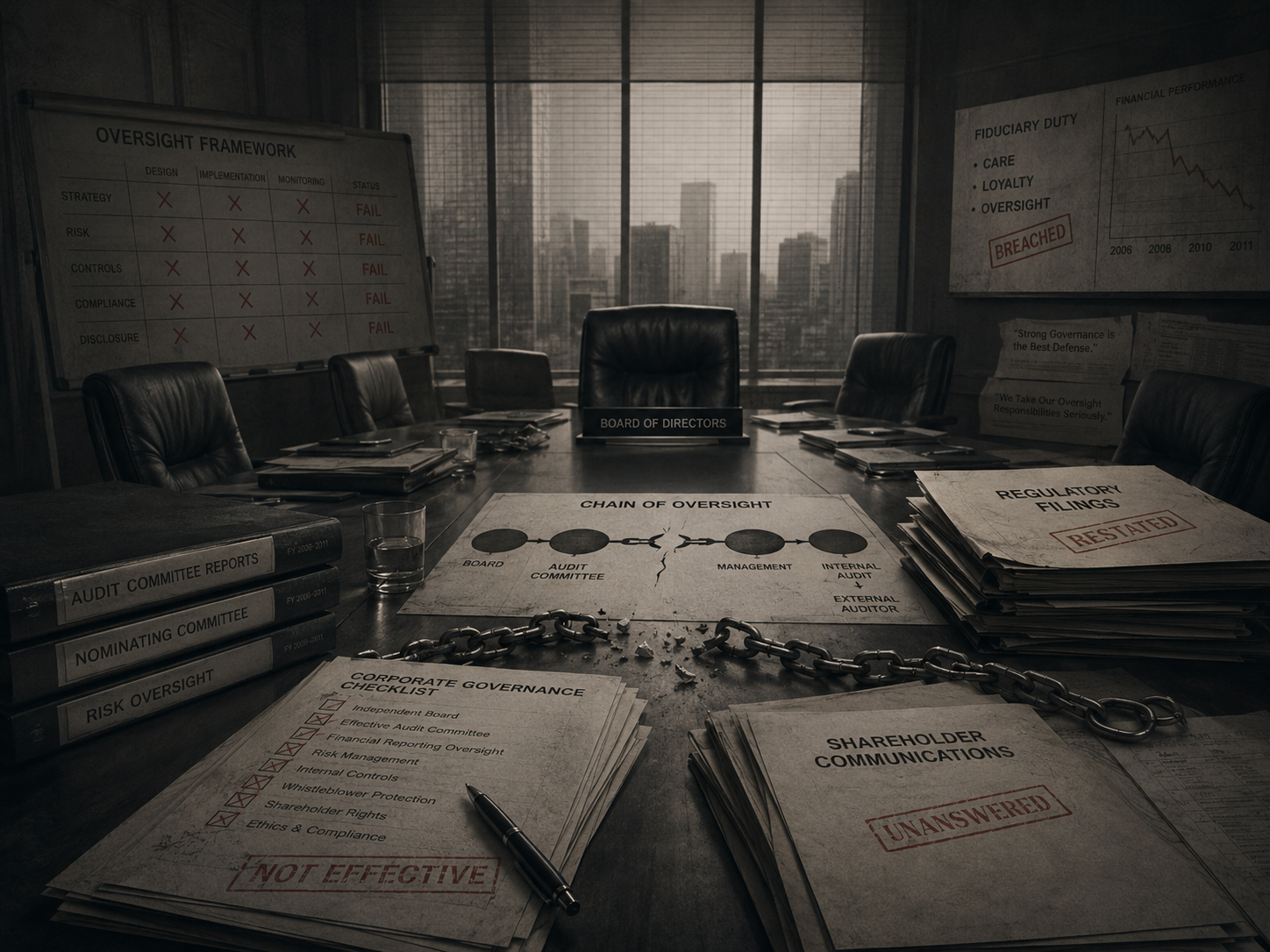

Governance Failure

At the center of the Olympus scandal were audit committees, directors, auditors, outside advisers, banks, legal and accounting professionals, and internal reporting channels. Governance is not a diagram. It is whether bad news can travel upward without being buried.

The issue was not only that accounting entries were made. It was that the structure allowed difficult questions to be delayed, deflected, or punished.

Source Notes

This page is based on Financial Services Agency statements, Olympus third-party investigation materials, exchange disclosures, enforcement actions, legal proceedings, major domestic and international reporting, and corporate-governance research. Where figures or responsibility boundaries differ across sources, the file separates established facts from interpretation.

- Financial Services Agency statements and market-fairness comments

- Olympus third-party investigation report and company disclosures

- Tokyo Stock Exchange, Securities and Exchange Surveillance Commission, and legal materials

- Major Japanese and international reporting from 2011 onward

- Corporate-governance scholarship and analysis